IBA, as the premier business brokerage firm in the Pacific Northwest, is firmly established as a respected professional service firm in the legal, accounting, banking, mergers & acquisitions, real estate, and financial planning communities. Periodically, we will post guest blogs from professionals with knowledge to share for the good of owners of privately held companies & family owned businesses. The following blog has been provided by Joe DiDomenico:

Involving Retirement Plan Funds in Privately Held Business Mergers and Sales

The involvement of retirement plan funds in private stock or private debt can be a valuable tool for stakeholders in mergers or sale transactions of privately held companies. Like most business opportunities, there are rules and constraints. You also need to weigh the pros and cons.

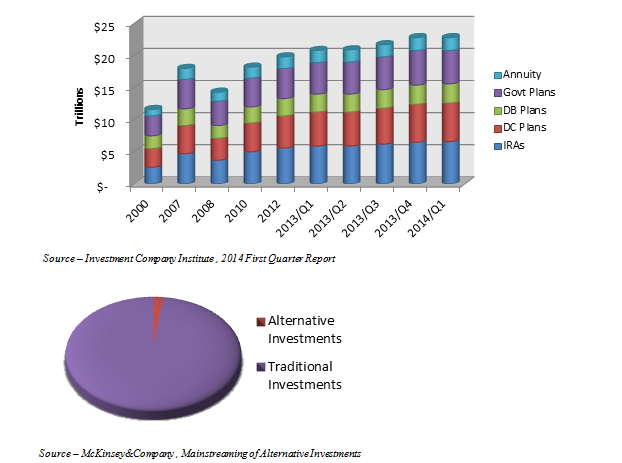

Many people are unfamiliar with the rules governing private investments in retirement plans, including some sophisticated financial professionals. The reason for this is that 98% of the $23 trillion in retirement plan assets in the US are registered traditional investments. These assets are held at traditional custodians who are in the business of facilitating Wall Street-type securities. So for the most part, people have not had to learn the rules.

The reach and strength of Wall Street to gather assets has been tremendous, but this is beginning to change as more independent financial advisors are introducing alternative assets classes to their clients, and more professional service providers are comfortable advising on

private investments. In addition, retirement plan cash is considered more often now as a source of liquidity for privately held business transactions. So the $23 trillion is increasingly becoming an opportunity for people selling their privately held businesses. The US Securities and Exchange Commission states in its 2009 report titled Asset Allocation 101:

“Stocks, bonds, and cash are the most common asset categories. These are the asset categories you would likely choose from when investing in a retirement savings program or a college savings plan. But other asset categories – including real estate, precious metals and other commodities, and private equity – also exist, and some investors may include these asset categories within a portfolio.”

The Rules:

The ERISA act passed in 1974 created the opportunity for retirement plans. The act was designed to afford a tax advantaged way for the American people to save for their retirement, and relieve some pressure from Social Security. Congress wanted to be certain it wouldn’t have a few unintended consequences, so investment permissibility rules were put in place. These rules are defined by US Treasury Regulations (26 U.S. Code § 4975). The rules are detailed and governed by the US Department of Labor and policed by the IRS. Each has its roots from one of three major concerns.

Unfair Competition

• Many Congressman during the enactment of ERISA owned businesses that were not owned in tax advantaged accounts and they did not want to allow competitors to have a pricing advantage over their family dynasty.

Benefiting Today’s Lifestyle

• ERISA was intended to encourage saving for retirement, not reduce taxes on spending.

- If the rules allowed IRA owners the ability to enjoy funds in IRA accounts too much, they would never take a taxable distribution. They would simply enjoy the things the IRA buys.

- Any activity that could be considered a hobby of a retirement account owner, or is a collectible item, is also not an allowed investment.

Reducing Estate Taxes

• It would be too tempting for some people to pass wealth between generations by giving preferential treatment on transactions to family members, thus avoiding estate taxes.

- To avoid having to police every transaction in retirement plans, it became off limits to conduct business with lineal ascendants and lineal descendents of a retirement account owner.

These rules can be a constraint for someone who wants their retirement plan to invest in a company that they will be running themselves. This would be a listed transaction by the IRS and you need to dot your I’s and cross your T’s. But it is possible with a “Rollover as Business Start-up” or (ROBS) Plan. It is also a constraint for a company owner to sell their company to a retirement plan owned by a family member. There are a few ways to work within the rules and still accomplish these things, to some degree. These two situations should be evaluated by a professional first.

Not all transactions done in a retirement plan are tax advantaged. If your IRA were to buy a business with $1 down and borrow $1 million, then the income and gains from that investment would pay taxes on the leveraged portion. So 99.99% of it would be taxed at the Trust tax rates, which hits the 39.6% tax bracket at $11,950 in income. Also, any loans that a retirement plan receives to purchase an asset may not be recoursed back to the plan owners. Most traditional bank financing requires this, but there are lenders out there that specialize in providing loans to retirement plans.

The benefits of investing in privately held companies that are not leveraged, not purchased from family members, and not run by the owners of the plan are very good. If a Roth IRA for example, has ownership in a privately held company, it is possible to have all of the income that the IRA generates from that company to go to the IRA owner tax free for his or her lifetime.

About the Author:

Joe DiDomenico is a Certified IRA Services Professional and is the co-founder of PrimeFund®, a Bellevue, WA company that provides self-directed retirement plan services.