IBA, as the premier business brokerage firm in the Pacific Northwest, is firmly established as a respected professional service firm in the legal, accounting, banking, mergers & acquisitions, real estate, and financial planning communities. Periodically, we will post guest blogs from professionals with knowledge to share for the good of owners of privately held companies & family owned businesses. The following blog has been provided by Carrie Callaway Cardy & Michele Gendron of Wells Fargo.

So, You Want To Be Your Own Boss?

By: Carrie Callaway Cardy and Michele Gendron, SBA Lending Specialists, Wells Fargo

Well, of course you do! Who wouldn’t? One great way to get there is to buy an existing, established business. So, where do you start? Below, we’ve laid out answers to some of the most common questions people ask when looking into financing a business acquisition:

How can I finance the purchase of an existing business?

The most common reason people state for not owning their own business is the lack of a down payment and little start-up capital. But the good news is banks are lending money for businesses and a loan backed by the U.S. Small Business Administration (SBA) is a great option.

The SBA offers guarantees on loans made through qualified lenders with terms that are very appealing to small business owners. Some highlights include: low down payments, long term loans, no prepayment penalties, and competitive interest rates and fees. Look for a bank that is part of the SBA “preferred lenders program” (PLP) as PLP providers have been delegated by the SBA for loan approvals, closing and servicing authority. Wells Fargo is an example of a PLP lender and happens to be the nation’s #1 SBA Lender for the 6th straight year.

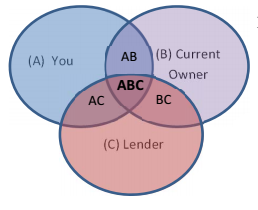

What does the art of the deal look like and who’s involved?

It’s a combination of players. Usually, a business broker or attorney will assist by helping you (A) and the current business owner (B) come to terms of agreement on the sale. This will usually be in the form of a Letter of Intent (LOI). Often, even before this is completed the lender (C) will work to pre-qualify you and the business. The final part of the deal comes together at point ABC (see graphic) – a partnership between you, the current owner, the lender and the advisors. What does the business need to do for you?

The business needs to generate enough cash flow to:

1 – Pay you a reasonable salary :

2 – Repay the lender(s)

3 – Have some cushion for the normal ups and downs of a business

So, how can you tell if the business will meet #1, 2 and 3? This comes in examining the cash flow of the business based on the financial documents supplied by the seller and/or accountants. Good news! Your lender can help you determine what documents are needed for this analysis and walk you through the requirements for an approval.

What will the financing look like?

Remember the ABC point above? All three parties can be expected to contribute toward the financing package:

(A)– A buyer can expect to contribute at minimum a 15% down payment (depending on the lender, creditworthiness of the buyer, and the business history) towards the purchase price, plus additional reserves for working capital (for day-to-day operations.)

(B)– The seller can provide financing toward project, usually 5-15%

(C)– The lender will provide the remainder of the financing needs

To get started in the process, the lender will give you a list of items needed, help you with the application process and work with an underwriter for an approval. Once you are approved and ready to move forward with the purchase, the lender will engage a third-party professional to complete a business valuation report and work with you to secure a closing.

When you buy a business, you take over an operation that’s already generating cash flow and profits. You have an established customer base, reputation and employees who are familiar with all aspects of the business. And you don’t have to reinvent the wheel. Plus, you won’t be alone throughout the process. So, are you ready to be your own boss?

If so, please contact one of these Wells Fargo SBA specialists who are happy to assist you in learning about the next steps.

Carrie Callaway Cardy

206-402-2917

[email protected]

Michele Gendron

425-407-3657

[email protected]