Rules of thumb often do not reflect the true market value of a professional practice being sold. For example, caution is advised when using published rules of thumb for valuing a veterinary practice like “a veterinary hospital should be valued at 76% of the prior year’s gross revenues” or “four times net income”. These appear to be an easy way to get a fair market value, however, as any veterinary practice owner knows, no two practices are exactly alike in terms of labor expense, occupancy costs, community demographics, etc. and therefore instinctively sellers & buyers should know that they will have different fair market values.

The Internal Revenue Service has determined that value of a business is comprised of two primary elements – tangible and intangible assets. Tangible assets (physical items) are equipment, furnishings, fixtures, leasehold improvement, client records, websites, products for sale and supplies. Intangible assets (the going concern) are location, community demographics, parking, accessibility, quality of patients, market identity, office systems, quality of staff, practice revenues, types of revenues, and discretionary net income.

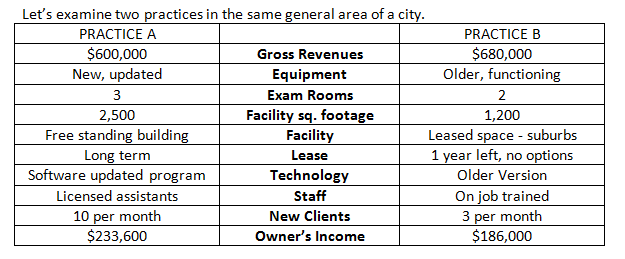

The rule of thumb “for national sales of veterinary practice” is 76% of the prior year’s gross revenues. Which of the above practices should have a higher value using this valuation model? Is the value of one practice potentially greater than 76% of the prior year’s years gross revenue?

Rules of thumb do not take any differences into consideration, but only look at the average final sale price. Each of the factors identified in the chart can increase or decrease the value of the price a knowledgably purchaser is willing to pay. A generic valuation model also does not take into consideration motivation for acquisition or sale. A practice targeted for acquisition by a corporate buyer in a specific geographic location may sell for a premium above market value while a practice being sold by a doctor facing health issues may sell at a discount from market value. A valuation model based solely on annual collections would value “Practice B” greater than “Practice A”. To a buyer, “Practice A” is a higher quality practice and a better value. The evaluation of professional practices is subjective science. It is recommended that a veterinarian considering the sale of their practice consult with a business broker with the knowledge & experience required to correctly value the hospital.

The above blog was written by Michael Kovsky D.V.M. Dr. Kovsky is the Director of IBA’s Professional Practice division. He has successfully facilitated over 400 transactions since 1991.

IBA, the Pacific Northwest’s premier business brokerage firm since 1975, is available as an information resource to the media and the mergers & acquisitions community on confidentiality and any other subjects relevant to the purchase & sale of a business.